What a $90B Valuation Says About OpenAI's Traction and Revenue Growth

This is not about raising new funds, but pegging a new valuation

The Wall Street Journal reported earlier this week that OpenAI is seeking to sell shares that would value the company in the $80-$90 billion range. According to the article:

The startup, which is 49% owned by Microsft, has told investors that it expects to reach $1 billion in revenue this year and generate many billions more in 2024, people familiar with the discussion said.

The deal is expected to allow employees to sell their existing shares as opposed to the company issuing new ones to raise additional capital. OpenAI representatives have begun pitching investors on the deal, the people said, though it is possible the terms could change.

If true, this is an extraordinary insight into a 2-3x valuation rise since Microsoft invested a reported $10 billion at a $29 billion valuation in January. This type of valuation leap cannot be explained away by hype alone. There must be strong revenue traction above previous forecasts or a rise in the total addressable market (TAM) - probably both.

Rising Revenue

The first thing to consider is the revenue information. You may recall a December 2022 Bloomberg report that suggested OpenAI expected to generate around $200 million in 2023 and $1 billion in 2024. That time scale just moved forward one year. The expected revenue for this year is now five times greater than forecasted nine months ago. The ChatGPT moment is more than hype.

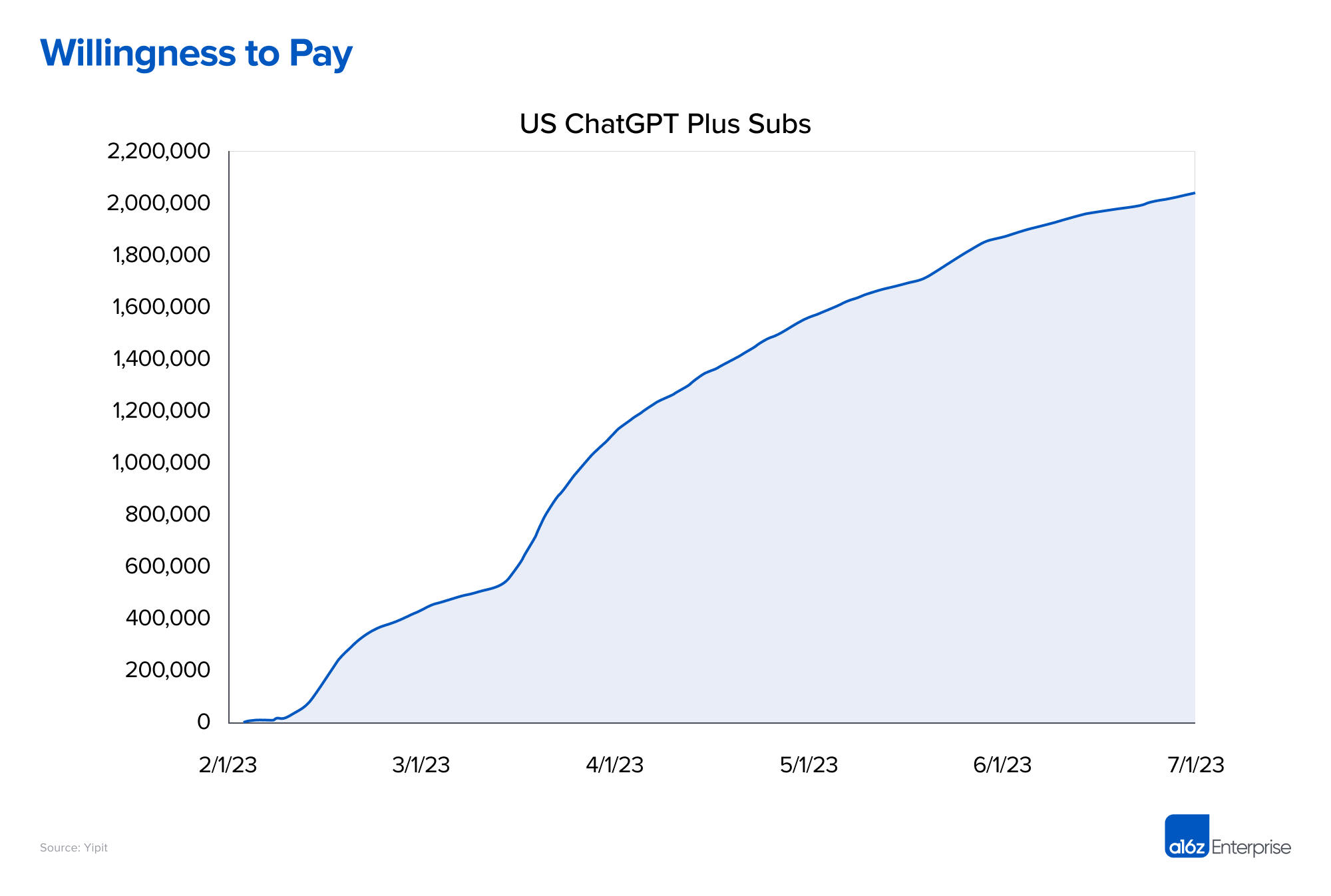

Synthedia reported recently that forecasts and musings of the death of OpenAI and ChatGPT were unfounded by market data. For example, we pointed to an a16z chart showing two million ChatGPT Plus subscribers as of July 2023 in the United States. That alone would be a $500 million annual revenue business just from a single application.

This revenue estimate is before considering the fees for companies directly accessing OpenAI’s API services. It is also before considering new revenue from the $60 per user per month cost of ChatGPT Enterprise. In addition, the global subscriber base of ChatGPT Plus may be closer to four million, which would be a billion-dollar run-rate business.

Of course, ChatGPT Plus wasn’t even available in the first quarter of 2023, and there was a ramp-up period. At most, that would account for about $500 million this year. The balance of the $1 billion is likely forecasted to come from ChatGPT Enterprise and the foundation model family of APIs.

There is an implication here for OpenAI and for the generative AI industry. Everyone knows that NVIDIA is generating a lot of incremental revenue from its chips optimized for AI workloads. OpenAI’s acceleration suggests there is significant revenue beginning to accrue at the foundation model and software layers. It is an open question how broadly this will spread throughout the industry. However, it does make the $4 billion investment by Amazon for a minority stake in Anthropic easier to understand.

Liquidity vs Cash Requirements

Another interesting element of the story is the fact that the company is not raising money but instead offering liquidity to employees. Since OpenAI does not intend to go public in the near term, it could be a long wait for employees to take advantage of the company’s early success.

This could also be interpreted as OpenAI moving beyond the point where it requires additional capital. That point is less clear. The article suggests that OpenAI intends to tap into investment markets again and this maneuver could set a new valuation price to be used in its upcoming funding round.

Valuations Don’t Matter, Except When They Do

There are readers of Synthedia that bemoan all of the talk about valuations as opposed to real value creation. They also suggest it cannot be used as a proxy for value creation because their is too much hype-fueled noise to be a reliable signal. However, it is a data point about how capital markets view the individual companies in the space today and over time the trend line will tell a more reliable story. OpenAI is much further along the business maturity curve than most of its peers. What was mostly noise is beginning to show a fair bit of signal.

Leaving the valuation aside, the fact that OpenAI is forecasting $1 billion in revenue this year is an very important point. Generative AI is not only a compelling technology; it is a technology that business and consumer users are willing to pay for. That data confirm the perception of value creation and the valuation is looking more like a lagging indicator.

Of course, this valuation float remains unverified. Maybe the valuation will be lower after the dust settles. That would be another data point or even signal in a sea of noise. Let me know what you think in the comments below. Agree? Disagree?

Amazon Reshuffles LLM Ecosystems with an [up to] $4B Investment in Anthropic

![Amazon Reshuffles LLM Ecosystems with an [up to] $4B Investment in Anthropic](https://substackcdn.com/image/fetch/$s_!MyW6!,w_1300,h_650,c_fill,f_webp,q_auto:good,fl_progressive:steep,g_auto/https%3A%2F%2Fsubstack-post-media.s3.amazonaws.com%2Fpublic%2Fimages%2Fee28339c-609f-42e9-8986-b05928518712_1920x1080.jpeg)

Amazon will invest up to $4 billion in Anthropic and have a minority ownership position in the company. Anthropic and Amazon announced a new partnership today that includes the former committing to running its primary training and inference workloads on AWS, and the latter investing “up to $4 billion,” for a minority stake in the company. There is a lot …